Material Insight: The Dielectric Constant of PCB Materials

Material Insight: The Dielectric Constant of PCB Materials American Made Advocacy: What About the Rest of the Technology Stack?

American Made Advocacy: What About the Rest of the Technology Stack? It’s Only Common Sense: Great Ideas From John Mitchell’s Book on Hiring Habits

It’s Only Common Sense: Great Ideas From John Mitchell’s Book on Hiring HabitsMiddle East and Africa Server Market Hit by Declining Enterprise IT Budgets

September 28, 2015 | IDCEstimated reading time: 2 minutes

The Middle East and Africa (MEA) server market – comprising x86 and non-x86 servers – contracted 10% year on year in Q2 2015 to total 65,000 units, according to the latest figures from International Data Corporation (IDC). This decline can primarily be attributed to the poor political and socioeconomic conditions that have hampered a number of countries in the region; this was particularly notable in the x86 server market where a number of significant projects within the government sector were delayed. In revenue terms, the market remained flat as there was a slight increase in the number of higher-end servers sold during the quarter.

"Saudi Arabia and the UAE experienced very slow quarters, both in terms of x86 server units and revenue, primarily due to delayed budget rollouts, the traditional slowdown over Ramadan, and continuing uncertainty around falling oil prices," says Victoria Mendes, a research analyst for systems and infrastructure solutions at IDC Middle East, Africa, and Turkey. "Combined, these two countries suffered declines of 28% in volume and 21% in value year on year in Q2 2015. But despite the slowdown, the UAE did see a few deals take place in the government and financial sectors, while Saudi Arabia saw a big deal in the oil and gas industry."

The South Africa server market expanded 24% year on year in revenue terms as a result of some non-x86 deals in the banking and telecommunications sectors. The declining average price of x86 servers has resulted in an increase in the number of units being purchased.

Revenue in Turkey was up by around 20% year on year despite the market suffering a 10% decline in shipments. This anomaly can be attributed to the fact that several large-scale deals took place during the quarter. The market is also seeing improved uptake of virtualization technologies, which consume lesser server units than is the case in traditional datacenters.

HP retained top spot in the MEA server market with 42% share, followed by Dell with 27%. Lenovo saw its share shrink, but managed to hold onto third place. Cisco's shipments slowed a little year on year, but its revenue was up 31% over the same period thanks to the strong performance of its blade form factor.

Looking at the second half of 2015, IDC expects the MEA server market to experience a 4% increase in volume and a 6% decline in value year on year. The growth in units will be spurred by a number of significant deals that are expected to take place in key countries like Saudi Arabia, South Africa, and Nigeria. These deals will primarily be within the healthcare, government, financial services, and telecommunications sectors. The decline in the market's revenue will be driven by the fact that vendors like Huawei and Lenovo are offering servers that are almost 40% cheaper than the prices offered by the market's A-ranking vendors.

"Longer term, the outlook for the MEA server market makes for grim viewing, with single-digit growth rates forecast for the duration of IDC's five-year forecast period," says Mendes. "This represents a significant slowdown from the bumper double-digit growth rates seen in the past. The first half of 2015 has ascertained that the prevailing macroeconomic forces are having a negative impact on enterprise IT spending, and the server market is unlikely to escape the fallout."

About the Research

IDC's 'EMEA Quarterly Server Tracker' is a quantitative tool for analyzing the server market on a quarterly basis. The tracker includes quarterly shipments (both ISS and upgrades) and revenues (both customer and factory), segmented by vendor, family, model, region, country, operating system, price band, CPU type, and architecture.

Share on:

Suggested Items

SPEA Expands in Southeast Asia with New Subsidiary in Thailand

05/17/2024 | SPEASPEA, a global leader in automatic test equipment for the manufacturing of semiconductor, microelectronic and electronic devices, today announced the opening of its new subsidiary in Thailand. This expansion marks a significant step forward in SPEA's commitment to serving the growing Southeast Asian microchip and electronics market with leading-edge manufacturing machinery and equipment.

PCB Market Size to Grow by $29.06B from 2024-2028

05/17/2024 | PRNewswireThe global printed circuit board (PCB) market size is estimated to grow by USD 29.06 bn from 2024-2028, according to Technavio. The market is estimated to grow at a CAGR of over 6.6% during the forecast period.

AT&S 2024/25 on Growth Course Again

05/17/2024 | AT&SAT&S operated in a challenging market environment in the financial year 2023/24. After a strong second quarter, demand was relatively weak again in some market segments in the second half of the financial year.

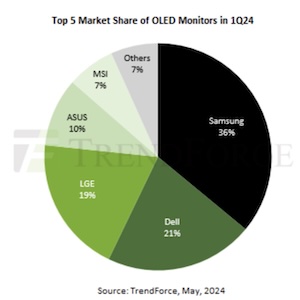

Shipments of OLED Monitors Hit 200,000 Units in 1Q24, Annual Forecast to Reach 1.34 Million

05/17/2024 | TrendForceTrendForce’s latest report reveals a robust start to 2024 for OLED monitors, with shipments reaching approximately 200,000 units in the first quarter—marking a YoY growth of 121%.

Magnachip Celebrates the Grand Opening of Magnachip Technology Company in China

05/16/2024 | MagnachipMagnachip Semiconductor Corporation celebrated the opening ceremony of Magnachip Technology Company, Ltd. (MTC) yesterday at its headquarters located in Hefei, China. MTC is a subsidiary of Magnachip, established on December 20, 2023, to expand the Company’s display driver IC and power IC businesses in China.